A. Background

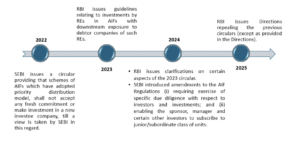

- TheRBI (Investment in AIF) Directions, 2025 (“Directions”), issued on July 29, 2025, are the latest in a series of regulatory interventions aimed at curbing risks associated with investments by regulated entities (“REs”) in Alternative Investment Funds (“AIFs”). These directions follow earlier circulars (“Old Circulars”) which restricted REs from investing in AIFs that, directly or indirectly, invest in their own debtor companies. A key concern underlying these moves has been the potential use of AIF structures for evergreening of loans and masking true credit risk. Simultaneously, SEBI has also acted, most notably through its circular dated November 23, 2022, which curtailed the use of the priority distribution model, and a circular dated December 13, 2024, which permitted certain investors to subscribe to junior/subordinate classes of units.

Chronology of key events:

Against this backdrop, this article presents a concise comparison of the key differences between the provisions of the Directions and the Old Circulars.

The Directions are applicable to the following REs:

- Commercial Banks (including Small Finance Banks, Local Area Banks and Regional Rural Banks)

- Primary (Urban) Co-operative Banks/ State Co-operative Banks/ Central Co-operative Banks

- All-India Financial Institutions (“AIFIs”)

1 Circular No. RBI/2023-24/90 DOR.STR.REC.58/21.04.048/2023-24 dated December 19, 2023 and Circular No. RBI/2023-24/140 DOR.STR.REC.85/21.04.048/2023-24 dated March 27, 2024.

2 Paragraph number 1.2.2 of the RBI’s ‘Master Directions on Fraud Risk Management in Commercial Banks (including Regional Rural Banks) and All India Financial Institutions’ provide the reference to AIFIs as follows:

“1.2.2 Export-Import Bank of India (‘Exim Bank’), National Bank for Agriculture and Rural Development (‘NABARD’), National Bank for Financing Infrastructure and Development (‘NaBFID’), National Housing Bank (‘NHB’) and Small Industries Development Bank of India (‘SIDBI’) as established by the Export-Import Bank of India Act, 1981; the National Bank for Agriculture and Rural Development Act, 1981;

- NBFCs (including Housing Finance Companies)

Since investments by REs were made in AIFs under the framework of the Old Circulars, the Directions seek to clarify the applicability of the old and new regulatory regime based on the funding status and timing of the commitment made by the RE in the AIF. The Directions establish a three-tier framework for determining which regulatory regime applies, as outlined below:

Applicable Framework | Nature of RE’s commitment in the AIF |

Old Circulars | The RE’s commitment to the AIF was fully funded as on July 29, 2025. |

Old Circulars or Directions | If an RE has (i) any unfunded portion of an existing commitment; or (ii) has entered into any new commitments prior to the effective date (i.e., January 01, 2026, or an earlier date determined by the RE in accordance with its internal policy). |

Directions | If an RE has made any new commitment in an AIF after January 01, 2026, or an earlier date determined by the RE in accordance with its internal policy. |

B. Comparative Snapshot – Old Circulars v. Directions

Particulars | Old Circulars | Directions |

Restrictions on investments by REs in AIFs | REs are prohibited from investing in AIFs which have direct or indirect downstream investments in a debtor company of the RE. | Individual contribution by an RE: Not more than 10% of the corpus of the AIF scheme. Collective contribution by all REs: Not more than 20% of the corpus of the AIF scheme. (please also see point immediately below) |

Provisioning requirements | REs need to undertake 100% provisioning when the AIF in which the RE is an investor makes a downstream investment in a debtor company of the RE and the RE is unable to liquidate their investments in the AIF within the timelines prescribed under the Old Circulars. Provisioning applies only to the extent of the investment by the RE in the AIF that is further invested by the AIF in the debtor company (and not on the entire investment of the RE in the AIF). Downstream investments exclude investments in equity shares of a debtor company but include investments in hybrid instruments. The term ‘hybrid instruments’ was not defined under the Old Circulars.

| If the RE contributes more than 5% of the corpus of an AIF which also has a downstream investment (excluding equity instruments) in a debtor company of the RE, then the RE shall be required to make 100% provision to the extent of its proportionate investment in the debtor company through the AIF subject to a maximum of the direct loan and/ or investment exposure of the RE to the debtor company. Equity instruments refer to equity shares, CCDs and CCPS, thereby, removing the ambiguity under the Old Circulars regarding hybrid instruments. Notably, optionally convertible instruments are not included in the definition of equity instruments. |

Deduction from Capital funds | Investments by REs in AIFs with priority distribution model is subject to full deduction from the RE’s capital funds. The capital deduction needs to take place equally from Tier-1 and Tier 2 Capital. | If the RE’s contribution is in the form of subordinated units, then it needs to deduct the entire investment from its capital funds proportionately from both Tier-1 and Tier – 2 capital (wherever applicable). This shall apply over and above the provisioning requirement discussed above. |

Exemptions | Investments by REs in AIFs through intermediaries such as fund of funds and mutual funds exempted from complying with the Old Circular. |

|

Debtor Company | Shall mean any company to which the RE currently has or previously had a loan or investment exposure anytime during the preceding 12 (twelve) months. | Shall imply any company to which the RE currently has or previously had a loan or investment exposure (excluding equity instruments) anytime during the preceding 12 (twelve) months. |

the National Bank for Financing Infrastructure and Development Act, 2021; National Housing Bank Act, 1987 and the Small Industries Development Bank of India Act, 1989, respectively (hereinafter referred to as ‘All India Financial Institutions or ‘AIFIs’.”

Further, RBI’s ‘Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity up to one year) Directions, 2024’ define AIFI as follows:

“All India Financial Institution (AIFI) shall include: (a) Export Import Bank of India, (b) National Bank for Agriculture and Rural Development, (c) National Housing Bank, (d) Small Industries Development Bank of India and (e) National Bank for Financing Infrastructure and Development.”

3 Under the December Circular, if the AIF made such a downstream investment in a debtor company, the RE had to liquidate its investment in the AIF within 30 days from the date of such downstream investment by the AIF. For REs which had already invested into such AIFs, the 30-day period for liquidation was to be counted from December 19, 2023.

C. Key Takeaways

The Directions represent a significant evolution in the regulatory framework governing investments by banks, NBFCs, and other financial institutions in AIFs.

One notable implication of the Directions is the imposition of a cap whereby REs collectively cannot invest more than 20% of the AIF’s corpus. This creates a practical urgency for REs looking to participate in AIFs, as they may need to move quickly before the available headroom is exhausted. Simultaneously, AIFs are likely to become more selective in onboarding REs, given that only a limited portion of their total corpus can be allocated to such investors. This may trigger greater competition amongst REs for participation in high-quality AIFs and push fund managers to rethink investor mix and fundraising timelines.

The Directions also provide a pragmatic roadmap to transition to the new regime based on the funding status and timing of commitments of the RE in the AIF, thereby avoiding disruptive implementation. The phased implementation approach beginning January 1, 2026 (or earlier if adopted by REs) provides sufficient time for REs to align their investment strategies with the new requirements.

Authors

Leelavathi Naidu, Senior Partner, IC RegFin Legal

Harsh Dilip Kothari, Partner, IC RegFin Legal

Siddhanth Sharma, Associate, IC RegFin Legal

Disclaimer: This document has been created for informational purposes only. Neither IC RegFin Legal Partners LLP nor any of its partners, associates or allied professionals shall be responsible / liable for any interpretational issues, incompleteness / inaccuracy of the information contained herein. This document is intended for non-commercial use and for the general consumption of the reader and should not be considered as legal advice or legal opinion of any form and may not be relied upon by any person for such purpose. You may read more about us at RegFin Legal and reach out to us at frp@regfinlegal.com.